Secure And Fair Enforcement Banking Act - H.R.1595

Banks and credit unions could provide financial services to state-authorized cannabis businesses without federal penalties under a modified version of H.R. 1595.

The bill is intended to make it easier for marijuana dispensaries and growers — as well as real estate owners, law firms, and other businesses that engage with them — to access the banking system instead of relying on cash transactions.

“Only Congress can provide the certainty financial institutions need to start banking legitimate marijuana businesses — just like any other legal business — and reduce risks for employees, businesses and communities across the country,” Rep. Ed Perlmutter (D-Colo.), the bill’s sponsor, said in a March 7 news release.

Some analysts said the industry could grow to $80 billion in annual sales by 2030, Bloomberg Law reported.

While several Republicans on the House Financial Services Committee opposed the measure at a markup earlier this year, the modified version of the bill slated for floor action includes provisions supported by some Republicans that would:

- Bar financial regulators from pressuring banks to drop clients such as gun retailers and payday lenders that were targeted under an Obama-era program.

- Add banking protections for legalized hemp businesses.

Further revised bill text posted Sept. 24 includes a cost-offsetting provision that would reduce by $4 million the combined amount of surplus funds held by Federal Reserve Banks. As under current law, any amount in excess of the cap would be transferred to the Treasury general fund.

Federal vs. State Laws

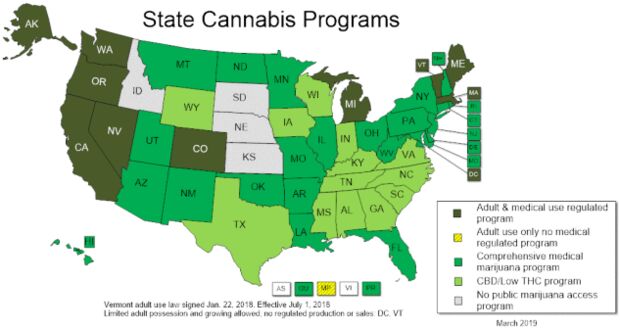

Most states have authorized the use of marijuana for medical or recreational purposes, but it’s still a prohibited substance under the federal Controlled Substances Act.

As a result, banks and other depository institutions can be penalized under federal money laundering laws for accepting deposits from a cannabis-related business. They’re also required to file Suspicious Activity Reports for transactions that could involve proceeds from marijuana sales.

Source: National Conference of State Legislatures

Under Barack Obama’s administration, the Treasury Department’s Financial Crimes Enforcement Network (FinCEN) issued guidance describing how banks could work with state-authorized marijuana businesses, while still complying with federal requirements to report suspicious transactions. The department told lawmakers in January 2018 that its guidance remained in effect, even under the stricter marijuana enforcement standards issued by former Attorney General Jeff Sessions.

“Notwithstanding the FinCEN guidance remaining valid, many financial institutions remain reluctant to serve cannabis-related legitimate businesses, and many of those businesses continue to have little to no access to traditional banking services,” according to a report on the bill from the House Financial Services Committee.

Pot businesses can’t accept credit card payments, deposit their profits, or write checks, and they’re a “soft target” for robberies, the committee wrote.

Other companies that sell products and services to those businesses have lost access to payment processors run by PayPal Holdings Inc. and Square Inc., according to a Feb. 12 memo from House Financial Services Committee majority staff.

Safe Harbor

The bill would shield banks, credit unions, payment processors, and insurers from federal regulatory and enforcement actions if they provide services to a cannabis-related business or its employees in a state, locality, or tribal area that legalized marijuana sales.

Federal banking regulators — including the Federal Deposit Insurance Corporation, National Credit Union Administration (NCUA), Office of the Comptroller of the Currency (OCC), Federal Reserve, and Treasury Department — couldn’t take adverse actions such as limiting a bank’s deposit insurance or encouraging it to cancel an account tied to a marijuana business or employee. They also couldn’t penalize new banks applying for charters or other banking privileges.

Covered financial institutions, as well as regional Federal Reserve Banks and Federal Home Loan Banks, also would be shielded from civil and criminal penalties for providing services to a cannabis company or investing any related income.

The modified text slated for floor action would expand the safe harbors to cover businesses that sell hemp, which was legalized by the 2018 farm bill (Public Law 115-334), as well as hemp-derived cannabidiol (CBD) products.

Guidance

Within 180 days of the bill’s enactment, banking regulators in the Federal Financial Institutions Examination Council would have to issue guidance and examination procedures for banks that provide services to cannabis businesses.

The Treasury Department would have to ensure that its suspicious activity reporting guidance complies with the measure. The Government Accountability Office would have to study how banks flag suspicious transactions for individuals or companies that engage with transnational criminal organizations in states with cannabis programs.

The modified text would also require banking regulators to issue guidance confirming that financial institutions can provide services to businesses that sell hemp and related products.

Terminating Bank Accounts

The modified text would bar regulators from asking or ordering banks or credit unions to terminate accounts based solely on a customer’s reputation.

Federal banking agencies would have to present a written notice to the financial institution that identifies the “valid reason” for terminating a specific account or group of accounts, as well as any laws that have been violated by the account holder.

The notification requirement wouldn’t apply if the targeted accounts or customers are:

- Involved in financing terrorism.

- A threat to national security.

- Associated with Iran, North Korea, Sudan, Syria, or any other country designated as a state sponsor of terrorism.

Financial institutions would have to tell customers why their accounts were closed, though institutions and agencies would be barred from providing such notifications if there’s a national security threat or if disclosure could interfere with a criminal investigation.

The provision comes from previous Republican-sponsored measures, such as H.R. 2706 in the 115th Congress, that were introduced in response to an Obama-era initiative called “Operation Choke Point” that was intended to stop fraudulent companies from accessing the banking system. Many Republicans raised concerns that the initiative, which is no longer in effect, could have cut off banking services for legitimate businesses such as gun retailers.

Marijuana Business Diversity

Banking regulators would have to provide Congress with an annual report on financial services accessed by minority-owned and women-owned cannabis businesses, as well as recommendations for expanding access.

GAO would have to study barriers to marketplace entry for those businesses.

Budget Effects

The Congressional Budget Office hasn’t published a cost estimate for the modified bill.

Implementing the committee-approved version — without the hemp or Choke Point-inspired provisions, or the cost-offsetting language — would have reduced the deficit by a net $2 million from fiscal 2019 through 2029, according to a May 24 cost estimate.

CBO said the measure would increase mandatory spending to resolve failed banks and credit unions that hold deposits from cannabis businesses. That spending would be offset by assessments levied on insured financial institutions, for a net $4 million reduction in mandatory spending.

Banking regulators would incur costs to develop guidance and examination procedures and issue reports. Costs incurred by the OCC and the NCUA would increase mandatory spending, but those agencies would collect premiums and fees to offset their costs, resulting in a net increase of $1 million. Costs incurred by the Fed would reduce revenue by $1 million.

Costs incurred by other agencies would increase spending subject to appropriation by less than $500,000 from fiscal 2019 through 2024.

CBO said the bill could impose a private-sector mandate if regulators issue banking guidance that’s stricter than current regulations. The measure also would impose a mandate by limiting a plaintiff’s right to sue a financial institution that provides cannabis banking services. CBO said it couldn’t determine whether those costs would exceed the private-sector threshold under the Unfunded Mandates Reform Act, which is $164 million in 2019 and is adjusted annually for inflation.

The measure also could increase a private-sector mandate if banking regulators increase their fees. CBO said the increase would be about $2 million from fiscal 2019 through 2024.

The bill doesn’t contain intergovernmental mandates.

Group Positions

Groups that SUPPORTED an earlier version of the bill included the American Bankers Association (ABA), American Land Title Association, American Property Casualty Insurance Association, Credit Union National Association (CUNA), Electronic Transactions Association, Independent Community Bankers of America, Independent Insurance Agents and Brokers of America, Law Enforcement Action Partnership, Mid-Size Bank Coalition of America, National Association of Attorneys General, National Cannabis Industry Association, and Real Estate Roundtable, according to the committee report. Many of the groups also reported lobbying on marijuana banking this year.

“Without congressional action, a significant portion of economic activity, including those businesses with only indirect connections to the cannabis industry, such as vendors, suppliers, and utility companies, risk being marginalized from the financial system in states with legal cannabis industries,” ABA and CUNA wrote in a March 25 joint letter.

Some banks may continue avoiding marijuana businesses until cannabis is legalized at the federal level, Bloomberg Intelligence analyst Nathan Dean wrote.

Smart Approaches to Marijuana (SAM) OPPOSED the measure.

“This bill is nothing more than a backdoor attempt at legalizing marijuana,” SAM President Kevin Sabet said in a March 28 news release.

“There will be little left to stop the industry from metastasizing into the next Big Tobacco,” he said.

Several groups urged Congress to delay action on the measure and instead take up legislation (H.R. 3884) to decriminalize marijuana at the federal level and make other comprehensive changes.

“The banking bill does not solve the underlying problems of marijuana prohibition — namely, that many people of color have been saddled with criminal records for a substance that is now legal in many states, and that communities have been shut out of the emerging and booming marijuana industry,” wrote the American Civil Liberties Union, Center for American Progress, Drug Policy Alliance, Human Rights Watch, and Leadership Conference on Civil and Human Rights in a Sept. 17 letter.

Previous Action

The House Financial Services Committee amended and approved the bill, called the “Secure And Fair Enforcement Banking Act” or “SAFE Banking Act,” by a 45-15 vote on March 28. Eleven Republicans joined with Democrats to back the measure.

The measure was also referred to the House Judiciary Committee, which agreed to forgo consideration, according to the committee report.

Perlmutter introduced the measure on March 7 and it had 206 cosponsors, including 26 Republicans, as of Sept. 24. He has introduced similar legislation in every Congress since 2013; none of his previous measures got a floor vote.

Senate Banking, Housing and Urban Affairs Chairman Mike Crapo (R-Idaho), who represents one of the few states without a cannabis program, said he planned to advance marijuana banking legislation following a July hearing on the issue. The committee hasn’t voted on a measure (S. 1200) introduced April 11 by Sen. Jeff Merkley (D-Ore.). That bill had 33 cosponsors, including five Republicans, as of Sept. 24.